The financial landscape in Malaysia is undergoing a significant transformation, driven by the widespread adoption of smartphones and the increasing comfort with digital transactions. In this evolving environment, loan applications, commonly known as loan apps, have emerged as a prominent feature, offering quick and accessible personal financing solutions to a broad spectrum of the population. As a financial expert, my aim is to provide a comprehensive guide to understanding this dynamic sector, ensuring that Malaysian consumers are well-informed and empowered to make prudent financial choices.

Current Digital Lending Market in Malaysia

Malaysia's digital lending ecosystem has experienced explosive growth, particularly in recent years. As of 2025, the market boasts over forty licensed online loan providers, all offering personal financing solutions primarily through mobile applications. This expansion is deeply rooted in the nation's high smartphone penetration, which stands at an impressive eighty-eight percent among adults, coupled with a growing comfort with digital banking services. The year 2024 alone saw a significant increase in licensed online money lenders, underscoring the rapid pace of development in this sector.

These fintech platforms cater to a diverse array of financial needs, ranging from immediate salary advances to small-scale microloans, and even extending to Shariah-compliant financing options. The availability of such varied services reflects a market that is responsive to the specific financial requirements of different consumer segments. This digital shift provides a convenient alternative to traditional banking channels, especially for individuals seeking swift access to funds.

The rapid growth also highlights Malaysia's progressive stance on financial technology, fostering an environment where innovation can thrive while still emphasizing the importance of a structured regulatory framework. This balance is crucial for ensuring stability and protecting consumers within the burgeoning digital finance space.

Understanding Loan Products, Rates, and Terms

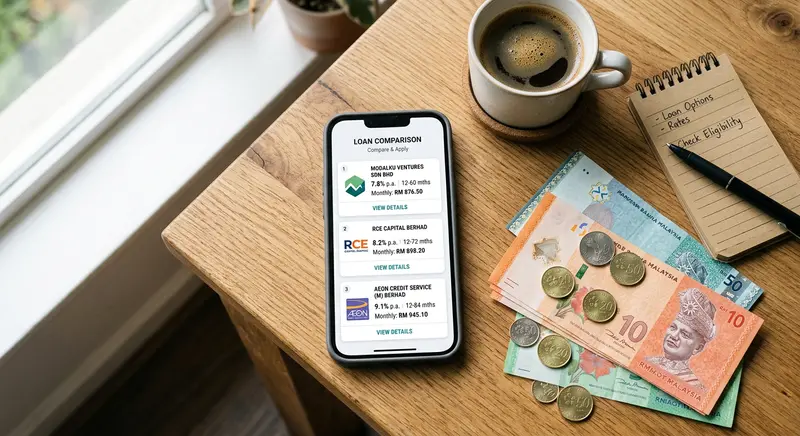

Loan apps in Malaysia offer a variety of products, each designed to meet specific financial situations. Understanding the details of these offerings, including interest rates, loan amounts, and repayment terms, is critical for any potential borrower.

Typical Loan Offerings and Amounts

- Salary Advances: These are usually smaller loans designed to bridge short-term cash flow gaps until the next payday.

- Microloans: Slightly larger than salary advances, microloans cater to small personal expenses or emergency needs.

- Personal Financing: These loans can range in size and are often used for larger expenses like education, home renovations, or debt consolidation.

- Shariah-Compliant Financing: For those who prefer or require it, several platforms offer financing options that adhere to Islamic principles, avoiding interest-based transactions.

While specific loan amounts will vary greatly by provider and the borrower's creditworthiness, microloans and salary advances typically involve smaller sums, often in the hundreds to a few thousand Ringgit. Larger personal financing options can extend to tens of thousands of Ringgit, depending on the lender's policies and the applicant's financial standing.

Interest Rates and Repayment Terms

Interest rates are a primary concern for any borrower. In Malaysia's digital lending market, typical annual percentage rates (APRs) for licensed providers generally range from 3.78% to 18%. However, it is important to note that non-bank lenders, especially those offering instant access to funds, may command rates towards the higher end of this spectrum, or even slightly above, reflecting the increased risk and convenience they provide.

Repayment terms also vary significantly. Short-term loans like salary advances might require repayment within weeks, while personal financing options can extend to several months or even a few years. Consumers must carefully review these terms before committing to any loan. Understanding the full cost of borrowing, including any processing fees, late payment charges, and the total interest accrued over the loan period, is absolutely essential.

Always compare offers from different licensed providers. A seemingly attractive low monthly payment might hide a longer repayment term, ultimately leading to higher total interest paid. Transparency in these figures is a hallmark of responsible lending practices.

Regulatory Landscape and Consumer Safeguards

The rapid expansion of digital lending in Malaysia is meticulously overseen by two key regulatory bodies: the Ministry of Housing and Local Government (KPKT) and Bank Negara Malaysia (BNM). Their stringent regulations are designed to ensure market stability, promote fair practices, and, most importantly, protect consumers from predatory lending and fraudulent activities.

Roles of Regulators

- Ministry of Housing and Local Government (KPKT): This ministry is primarily responsible for licensing and regulating conventional moneylenders, which includes many of the online loan app providers. KPKT sets guidelines for interest rates, loan terms, and business conduct to ensure that these entities operate within legal and ethical boundaries.

- Bank Negara Malaysia (BNM): As the central bank, BNM's role is broader, encompassing the overall financial stability of the nation. It regulates banks and financial institutions, and plays a crucial role in overseeing new digital banking licenses and financial technology innovations. BNM also focuses on consumer financial education and protection across the entire financial services sector.

This dual oversight ensures that digital lending services are not only innovative but also secure and compliant with national financial policies. The regulations cover various aspects, including advertising standards, data privacy, and dispute resolution mechanisms. Consumers should always verify that any loan app they consider is indeed licensed by the appropriate Malaysian authority.

Consumer Protection Measures

Despite the regulatory efforts, consumer protection remains a paramount concern. The regulatory framework aims to mitigate several risks:

- Illegal Lenders: The biggest risk is dealing with unlicensed or illegal moneylenders (Ah Long), who operate outside the law and often resort to aggressive and unlawful collection practices.

- High Interest Rates: While regulated, some lenders might charge rates that, while legal, can be financially burdensome. Consumers must compare and understand the true cost.

- Hidden Fees: Transparency is key. Regulations aim to prevent lenders from imposing undisclosed charges or fees.

- Data Security: Loan apps handle sensitive personal and financial data. Regulators enforce strict data protection standards to prevent breaches and misuse.

Consumers are encouraged to be vigilant and report any suspicious or unethical practices to the relevant authorities. The robust regulatory environment is a significant advantage for Malaysian borrowers, providing a safety net that is not always present in less regulated markets.

Market Trends, Technology, and Future Outlook

The trajectory of Malaysia's digital lending market is marked by dynamic trends and continuous technological integration. The future outlook suggests further growth, driven by innovation and an evolving regulatory approach.

Technology Adoption and Mobile Money Integration

The foundation of digital lending's success in Malaysia is undeniably the high rate of smartphone penetration and the increasing ease with which Malaysians conduct financial transactions on their mobile devices. Loan apps leverage this technological comfort, offering seamless application processes, quick approvals, and direct disbursement of funds. This convenience is a major draw for consumers who need fast access to credit.

Furthermore, the integration with mobile money and e-wallet platforms is becoming increasingly sophisticated. Many loan apps now allow funds to be disbursed directly into e-wallet accounts, or enable repayments through these popular digital payment methods. This synergy creates a more interconnected and efficient financial ecosystem, reducing friction for users and making financial services even more accessible.

Artificial intelligence and machine learning are also playing a growing role, enhancing credit assessment models and personalizing loan offerings. This allows lenders to evaluate a broader range of data points beyond traditional credit scores, potentially extending credit to underserved segments while managing risk more effectively.

Future Outlook and Market Trends

The future of digital lending in Malaysia appears poised for continued expansion and diversification. Key trends include:

- Increased Personalization: Lenders will likely offer more tailored loan products based on individual spending habits and financial behavior, made possible by advanced analytics.

- Expansion into Underserved Segments: Digital lenders are uniquely positioned to provide financial access to small businesses, gig economy workers, and individuals with limited traditional credit histories.

- Enhanced Regulatory Frameworks: As the market matures, regulators may introduce further refinements to policies, focusing on areas like responsible lending limits, ethical data usage, and robust consumer complaint mechanisms.

- Green Financing Options: There might be an emergence of digital lending products focused on sustainable or environmentally friendly initiatives, aligning with global trends.

- Collaboration with Traditional Banks: We could see more partnerships between fintech lenders and traditional banks, combining the agility of loan apps with the stability and capital of established financial institutions.

The market is expected to remain highly competitive, fostering innovation and potentially driving down costs for consumers in the long run. However, vigilance regarding financial literacy and responsible borrowing will continue to be crucial.

Practical Advice for Malaysian Consumers

While loan apps offer undeniable convenience, responsible borrowing is paramount. Here are five practical recommendations for Malaysian consumers:

- Verify Lender Licensing: Always ensure the loan app provider is licensed by the Ministry of Housing and Local Government (KPKT) or Bank Negara Malaysia (BNM). You can check official websites or contact the authorities directly. Avoid dealing with any unlicensed entities, as they operate illegally and pose significant risks.

- Understand All Terms and Conditions: Before agreeing to any loan, thoroughly read and comprehend the interest rates, repayment schedule, all fees (including processing fees, late payment charges, and stamp duty), and any penalties for early repayment. Ask for clarification if anything is unclear.

- Borrow Only What You Can Afford to Repay: Assess your current financial situation realistically. Calculate your monthly income and expenses to determine if you can comfortably make the repayments without jeopardizing your other financial obligations. Over-borrowing can lead to a debt spiral.

- Compare Multiple Offers: Do not settle for the first offer you receive. Compare interest rates, terms, and fees from several licensed loan apps to find the most favorable deal that suits your needs. A small difference in interest rates can lead to substantial savings over the loan term.

- Protect Your Personal Data: Be extremely cautious about the personal and financial information you share. Only use reputable, licensed apps that clearly outline their data privacy policies. Never share your passwords or banking One-Time Passwords (OTPs) with anyone.

By following these guidelines, Malaysian consumers can leverage the convenience of digital lending services while safeguarding their financial well-being and avoiding potential pitfalls.